Is Cost Accounting Accelerating Your Decline?

A question for CFOs at Washington State critical access hospitals: could standard cost allocation be distorting your service line decisions at exactly the wrong time?

TL;DR

When a critical access hospital cuts a service line because it “loses money,” the decision rests on how costs were allocated. If overhead was spread across services using standard methods, the loss may be an accounting artifact. The overhead stays. The revenue disappears. I could be wrong about this, and I am looking for CAH finance leaders who can check my reasoning.

Washington State has a critical access hospital problem. Several CAHs are in financial distress, some facing closure. The conversations around this crisis tend to focus on declining volumes, deteriorating payer mix, and rising costs. Those are real pressures. I am not questioning them.

I am questioning something more specific: whether the cost accounting methods these hospitals use might be distorting the service line decisions they make under that pressure. And whether those distortions might be making things worse.

A hypothetical that may not be hypothetical

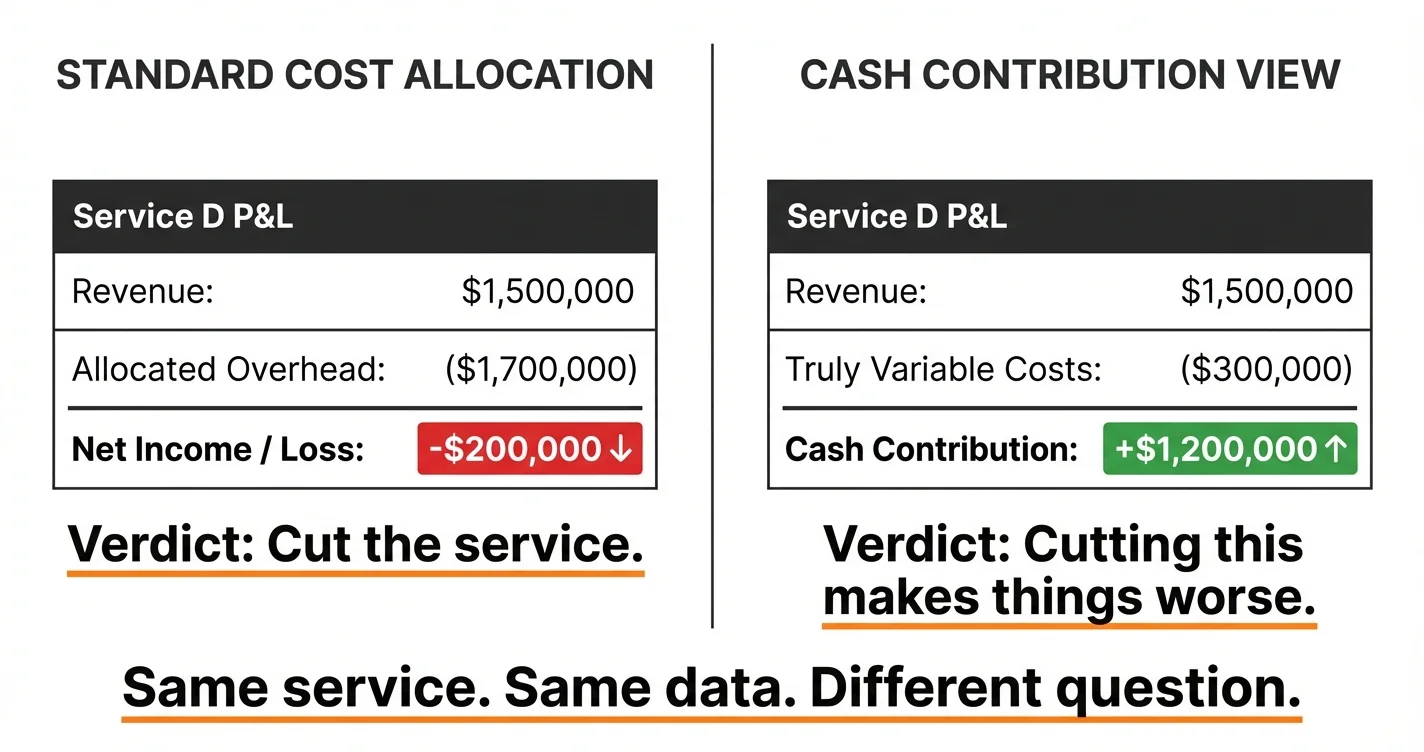

Consider a small critical access hospital running four service lines. The hospital has 10 million dollars in total operating expenses, of which 7 million is fixed overhead: building, administration, salaried staff, equipment depreciation, IT, compliance. These costs exist regardless of which services are offered.

The hospital’s cost accounting system allocates that 7 million across the four service lines, probably by relative volume, revenue, or some blend. One service line, call it Service D, generates 1.5 million in revenue. After its share of allocated overhead, the books show it losing 200,000 dollars a year.

The finance team recommends cutting Service D. The board agrees. The hospital is in distress and needs to stop the bleeding.

Here is what actually happens after the cut. The 1.5 million in revenue disappears. But the overhead that was allocated to Service D does not disappear with it. The building is still there. The administrators are still employed. The IT contracts are still running. Most of that allocated overhead simply gets redistributed to the remaining three service lines, making each of them look less profitable than they did before.

Meanwhile, the truly variable costs that went away with Service D, the supplies, the drugs, the per-case consumables, might have been 300,000 dollars. The hospital just lost 1.2 million in cash contribution (revenue minus truly variable costs) to eliminate a 200,000-dollar accounting loss.

The net effect on the hospital’s actual cash position: it got worse by roughly a million dollars.

Why this might hit CAHs harder

Large health systems have the same cost allocation problem, and I have been thinking about it in that context for a while. But critical access hospitals face a version of it that may be more damaging for a specific structural reason.

CAHs receive Medicare cost-based reimbursement: 101 percent of reasonable costs. That reimbursement model is literally built around cost accounting. Every strategic conversation gets filtered through “what does this cost us to deliver?” That is the question the entire financial feedback loop is designed to answer.

The question it is not designed to answer: “What cash does this service generate above its truly variable costs, and what happens to our fixed cost base if we eliminate it?”

The reimbursement model was designed to protect rural hospitals. But it may also be training their finance teams to think in exactly the framework that produces distorted service line decisions. When a CAH under financial pressure looks at its books and sees a service line “losing money,” the instinct to cut it is reinforced by the entire accounting structure the hospital lives inside.

And there is a compounding problem. When a CAH cuts a service line, it does not just lose the cash contribution from that service. It also shrinks the cost base that drives its cost-based reimbursement. Fewer services means fewer costs to report, which means lower reimbursement, which means tighter margins on what remains. The accounting that motivated the cut now produces a smaller hospital that is harder to sustain.

What I do not know

I do not know how widespread this dynamic is. I do not know whether CAH finance leaders are already accounting for it in ways that do not show up in the public conversation. I do not know whether the specific reimbursement mechanics of the 101-percent model change this calculus in ways I have not considered. I do not have direct experience running a CAH.

What I do have is a framework for thinking about fixed versus variable costs and how their misallocation distorts decisions, particularly under pressure. I have applied it in other settings. The pattern I am describing, where cutting a “losing” line makes the whole system worse, is well-documented in manufacturing and other industries. I believe the logic transfers to healthcare, and to CAHs specifically, but if I’m wrong, I want to hear about it.

The ask

If you are a CFO, controller, or finance director at a critical access hospital in Washington State, I would genuinely appreciate your perspective on this. Does this match what you see in your own financial reporting? Where does my reasoning break down? What am I missing about how cost-based reimbursement actually interacts with these decisions?

I am not selling anything here. I am trying to understand whether a pattern I have seen in other industries is showing up in the CAH crisis, and the only way to find out is to ask the people who live it.

You can reach me at john@common-sense.com, or find me on LinkedIn. I welcome the pushback as much as the agreement. Both help.